India’s Auto Component Industry

Can It Move Up the Global Value Chain?

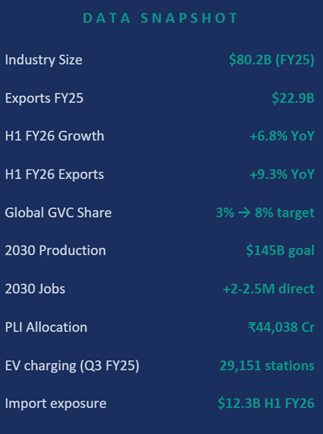

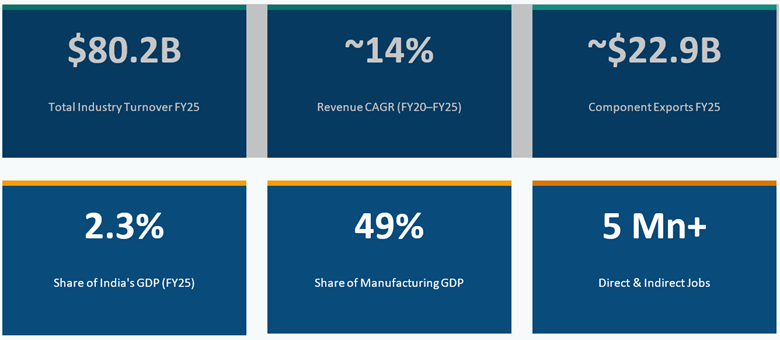

INDUSTRY AT A GLANCE

REVENUE GROWTH TRAJECTORY

| ~14% | CAGR FY20-FY25 |

| 6.8% | Growth in H1 FY26 |

| 10% | 5yr sector CAGR |

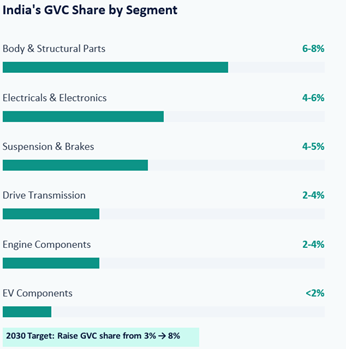

INDIA’S SHARE IN THE $700B GLOBAL COMPONENT MARKET

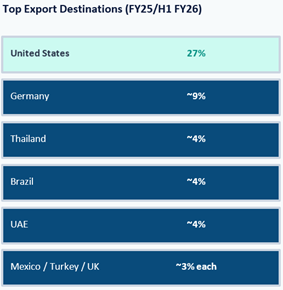

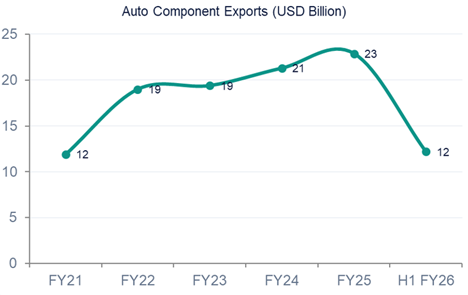

EXPORT PERFORMANCE & MARKET DESTINATIONS

WHAT COULD GO WRONG?

| RISK Slow EV adoption China price dumpingWeak semiconductor ecosystem Rare-earth dependency Delayed FTAsTechnology gap persists |

| POTENTIAL IMPACT Delays localisation and investment returns Margin pressure on Indian manufacturers Limits electronics value captureEV supply-chain vulnerabilityWeakens export competitiveness India remains low-value assembly hub |

THE CHINA+1 MOMENT IS RESHAPING AUTOMOTIVE MANUFACTURING

| RISK | POTENTIAL IMPACT |

| Slow EV adoption | Delays localisation and investment returns |

| China price dumping | Margin pressure on Indian manufacturers |

| Weak semiconductor ecosystem | Limits electronics value capture |

| Rare-earth dependency | EV supply-chain vulnerability |

| Delayed FTAs | Weakens export competitiveness |

| Technology gap persists | India remains low-value assembly hub |

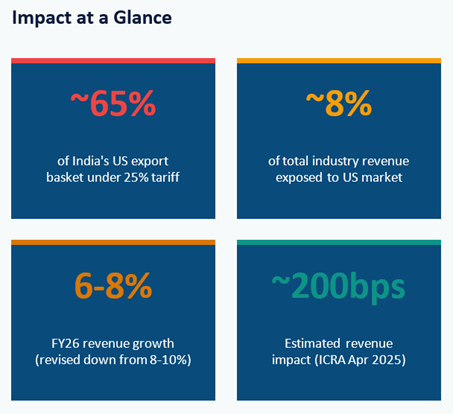

US TARIFF IMPACT: THE $6B QUESTION

In February 2025, the United States imposed a 25% tariff on the steel and aluminium content of automotive components, marking a significant increase in trade barriers for the sector. The scope of these measures expanded in March 2025 with the introduction of a 25% tariff on key automotive assemblies, including engines, transmissions, powertrain systems, and electrical components. In April 2025, a 26% reciprocal tariff on imports from India was announced; however, its implementation was partially deferred through a 90-day pause, during which a 10% ad valorem tariff remained in effect. Trade pressures intensified further in August 2025 when an additional 25% penalty tariff was imposed in response to India’s engagements with Russia, raising the effective tariff burden to as much as 50% for certain product categories. Greater clarity emerged in November 2025, when regulatory guidance standardized most affected categories under a uniform 25% U.S. tariff rate. More recently, the proposal in February 2026 to reduce the reciprocal tariff to 18% has been viewed as an encouraging development, signaling the potential for a more favorable trade environment and improved export competitiveness in the second half of FY26.

EV TRANSITION: DISRUPTION & OPPORTUNITY

| 480K | EV units sold India 2025 |

| 3M+ | Projected EV units by 2035 |

| 29,151 | Public charging stations Q3 FY25 (+78% CAGR) |

| $7B | Planned EV component localisation by FY2 |

AT RISK – ICE-Dependent Suppliers

- Engine & transmission component makers face existential risk as EV penetration rises

- India’s global share in drive transmission is only 2-4% low base to pivot from Over-reliance on CKD/SKD assembly models limits technology absorption 65% of component export basket goes to ICE-dependent OEM platforms

OPPORTUNITY – EV Component Growth

- Li-ion batteries, traction motors, BMS, power electronics, high-value segments to capture

- Wiring harnesses for EVs already a strength, low-voltage electronics growing fast

- PLI-backed $7B localisation plan targets battery cell manufacturing by FY28

- India’s EV market 6× growth projected by 2035, massive domestic pull factor

The China+1 Moment Is Reshaping Automotive Manufacturing

China+1 Diversification Is Accelerating

Global OEMs reducing dependence on China due to:

– trade tensions

– geopolitical risks

– supply-chain disruptions

– rising Chinese labour costs

Why India Is Benefiting?

– Large domestic auto market

– Low-cost engineering talent

– Policy support (PLI, PM E-Drive)

– Growing manufacturing ecosystem

– Lower geopolitical risk perception

STRUCTURAL BARRIERS TO VALUE CHAIN ASCENT

Cost Competitiveness Gap (~10% cost disadvantage vs. China)

- Energy costs 15-20% higher than Chinese competitors

- Logistics inefficiencies add ~3-5% to total cost

- Fragmented supply chains limit economies of scale

- 100% depreciation norms create 3.4% capital cost disadvantage (vs China’s 50%)

R&D & Innovation Deficit (India invests only 0.7% of GDP on R&D)

- vs. 2.4% in China and 3.1% in South Korea (World Bank 2023)

- India ranks 40th on Global Innovation Index (WIPO 2023)

- Limited automotive-specific patents filed domestically

- Low adoption of CAD-CAM, CNC machining & cleanroom technologies

Import Dependence ($12.3B imports in H1 FY26 (+12.5% YoY))

- China is top import source at ~23% of all component imports

- Critical rare earths, semiconductors largely China-sourced

- Engine parts and Body-in-White structures reveal key domestic gaps

- Rising trade deficit, imports now outpacing export growth

MSME & Precision Gap (MSMEs = 40% of revenue; Tier-1 status elusive)

- Most MSMEs operate below Tier-1 GVC supplier threshold

- India’s share in engine & steering systems only 2-4% globally

- Limited access to funding constrains technology upgrades

- Competition from Vietnam, Indonesia benefits from scale advantages

GOVERNMENT POLICY ARCHITECTURE

PLI: Auto & ACC Battery (₹44,038 Cr ($5.3B)) – PLI for automobiles (₹25,938 Cr) + ACC battery storage (₹18,100 Cr). 75 firms approved including Maruti, Hero, Tata, Ola, TVS. Total investment commitment: ₹74,850 Cr – 76% above target. Incentives up to 18% for advanced automotive technology (AAT) products.

FAME-II & PM E-Drive (₹66,000+ Cr mobilized) – EV charging infrastructure continues to expand rapidly across India. PM E-Drive allocates ₹2,000 Cr for 72,300 new EVPCS. Budget 2025-26 adds duty exemptions on Li-ion battery scrap and 35 capital goods for EV production.

GST Rationalisation (Dual rate: 5% & 18%) – GST rationalisation from Sep 22, 2025 simplified the tax structure. Small cars GST cut 28%→18%; EVs at 5%. Uniform 18% GST for ancillary components benefits MSME suppliers significantly on cost and compliance.

Critical Minerals Mission (25 minerals duty-exempt) – Budget 2025-26 provides customs duty exemptions to 25 critical minerals essential for EV batteries (lithium, cobalt, nickel). The Critical Minerals Mission established to build strategic reserves and reduce dependence on single-country supply chains.

NITI AAYOG VISION 2030: THE ROADMAP

| $145B | Production (from ~$80B today) |

| $60B | Exports (3× from $20B) |

| $25B | Trade Surplus (projected) |

| 8% | Global GVC Share (from 3% today) |

| 2-2.5M | New Direct Jobs Created |

Four-Category Strategic Framework for GVC Integration

- Emerging & Complex

- EV power electronics

- ADAS modules

- Battery management systems

- Autonomous tech sensors

Highest priority: build from ground up via FDI + PLI

- Conventional & Complex

- Engine systems

- Transmission modules

- Advanced steering systems

Upgrade precision manufacturing; close China gap

- Emerging & Simple

EV wiring harnesses

Low-voltage electronics

EV connectors & relays

Scale existing strengths into new EV formats

- Conventional & Simple

- Fasteners, brackets

- Filters & gaskets

- Castings & forgings

Maintain cost leadership; expand geographies

5 IMPERATIVES TO MOVE UP THE VALUE CHAIN

Technology Absorption – Close gaps in precision mfg, semiconductors & battery cells. FDI-led tech partnerships essential, avoid permanent CKD assembly trap.

MSME Upgrading – 40% of revenue in MSMEs must move from simple fabrication to R&D-capable Tier-1 quality. GVC Skilling Scheme + cluster-level capex support needed.

Energy & Logistics Reform – Close ~10% cost gap vs. China by reducing power costs and modernising logistics. Without this, PLI gains erode at the bottom line.

EV Bet Timing – Must avoid being trapped in stranded ICE investments while building credible EV component capabilities. $7B localisation plan must execute on schedule.

Trade Diplomacy – Leverage China+1 moment via FTAs with EU and US. Position India as reliable, rules-based supplier. Navigate WTO challenges from China on PLI schemes.

- Industry crossed $80B in FY25 with 14% CAGR, growth momentum is real

- 3% global GVC share massively understates India’s potential, 8% is achievable by 2030

- India retains relative tariff and supply-chain advantages as global manufacturers diversify sourcing beyond China.

- EV transition is the defining fork, who captures batteries & power electronics wins

- Execution on PLI, energy reform, and FTAs in 2025-28 is the decisive window